L R AS Published on Saturday 14 December 2019 - n° 302 - Categories:cells

Will N-PERT emerge in 2020?

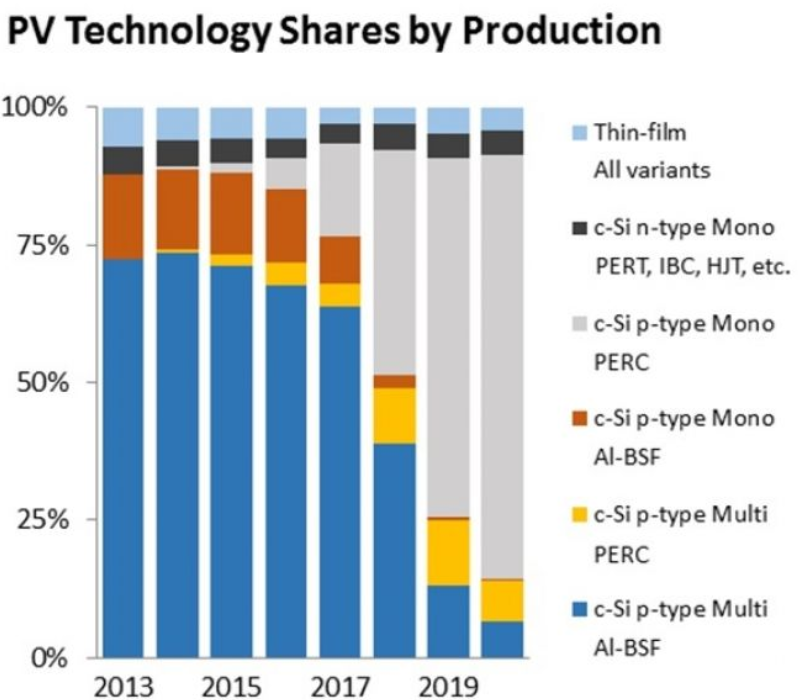

N-PERT could become an alternative to the current P PERC monosilicon standard which accounts for 80% of crystalline silicon production by 2020. The production of N mono-PERC cells is still limited by wafer supply.

Professionals are questioning the advisability of switching to type N. This hesitation is prompting the N-type cell production industry to leave production capacity below 10 GW in 2020. However, it would seem that the major manufacturers are going to change their attitude.

Two technologies have been put into service with type n: that of Sunpower with the back contact, and that of Sanyo/Panasonic with the heterojunction. These two companies have achieved a production capacity of one gigawatt, with cells that were not mass-produced. Yingly Green has developed a simplified technology (its Panda technology, also called n-PERT). LG Electronics has installed complex pilot lines. Some Chinese manufacturers have adopted LG's technology in the hope of being able to reproduce it with more common equipment. They soon realised that the performance level was lower than the P mono PERC type. Then Chinese manufacturers started heterojunction, hoping to lower production costs to a Chinese standard, which was much cheaper than Sanyo. By the end of 2019, heterojunction in China appears to be on hold.

The research teams are returning to the n-PERT platform which could appear in 2020/2021 under the impetus of JinkoSolar.

The production of cells dominated by mono P PERC could be at its peak: if one of the major manufacturers (JinkoSolar, Trina Solar, Canadian Solar, JA Solar, LONGi) starts to offer N-type products for unit volumes above 50 MW, the other major producers will have to align themselves and offer a comparable product, to show their technological competence.

JinkoSolar has installed a production capacity of one gigawatt type n. The other producers must also announce it. As heterojunction is considered to be a high risk, it seems that the n-PERT technology, also called TOPCon, is needed. Chinese manufacturers will make the investments in 2020-2021 in order to have significant capacity. As soon as JinkoSolar announces a capacity at 10 % of that of type p, type N will become widespread. The passage from 10 to 20 GW of production linked to n-PERT should be rapid, and should occur in 2021. If, in the meantime, it becomes viable to switch production lines to N-type wafers and to adapt production lines from mono-PERC to N-PERT, the transition will probably take place during the period 2023-2025.

Many obstacles remain. P-type proponents point out that the efficiency of P-type cells does not require conversion. This would overlook the advantages of the N type, which accepts high temperatures, or other operational advantages. Even if the efficiency gap is small, the gain for utilities will provide an incentive to convert.

So 2020 could be the pivotal year for the N-type. Jinko Solar is organising the changeover. We will see how success will spread to cell production. If this happens, it will only give new life to the heterojunction and the back contact, given the greater attention given to everything related to the N-type.

https://www.pv-tech.org/editors-blog/pv-celltech-2020-to-explain-why-n-pert-emerging-as-differentiated-play-for

PV Tech's blog of December 11th