L R AS Published on Monday 26 September 2022 - n° 417 - Categories:the American PV

A new era for made-in-USA solar

To reach the goal of 100% clean electricity by 2035, the US Department of Energy (DOE) estimates that solar energy would have to increase from 4% of the electricity supply today to 40% within 13 years.

Such growth will increase demand for all elements of the solar supply chain, from silicon to panels.

China and Chinese subsidiaries in Southeast Asia currently have a dominant share of the solar supply chain.

Securing a domestic supply chain to support the US clean energy transition has become increasingly crucial since the onset of the global energy crisis caused by Russia's invasion of Ukraine.

The solar industry is experiencing a critical shortage of silicon. Prices have reached highs not seen since 2011, partly due to the unexpected closure of a major manufacturer in Xinjiang for repairs. Xinjiang, in western China, is the region where nearly 50% of the world's silicon is produced.

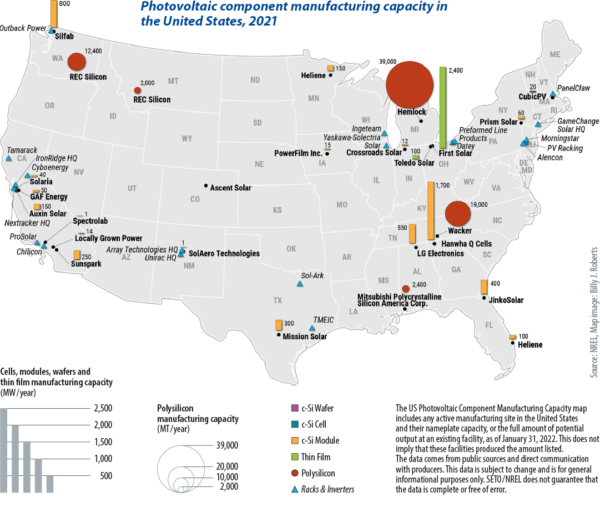

The state of photovoltaic production

The US has domestic silicon production capacity: Korea's Hanwha became the largest shareholder in REC Silicon in 2022. However, there is still no production of crystalline silicon ingots, wafers and cells in the US. There are manufacturers that assemble panels in the US.

Most of the major racking manufacturers in the US market produce exclusively in the US.

The two largest sellers of trackers, both globally and in the US, are the US-based NEXTracker and Array Technologies, which together account for 70% of tracker shipments in the US in 2020, and 46% of global shipments.

Inverters and power electronics are an example of where there is a global supply chain, as many components are manufactured around the world. Among the MLPE producers, Israel's SolarEdge has production facilities in Hungary, China and Vietnam. The second largest MLPE producer, Enphase, is headquartered in the US and has production facilities in China and Mexico.

The supply chain for inverters varies according to the type of machine. Large-scale inverters in the US are largely supplied by European and Japanese companies; residential inverters are sourced from the US and many other foreign countries.

The Inflation Reduction Act

Enacted in August, it provides $370 billion in spending on renewable energy and climate measures, including more than $60 billion for domestic manufacturing in the clean energy supply chain, which includes clean energy vehicles.

Cadmium telluride (CdTe) thin film PV technology was developed in the US. It accounts for about 20% of the panels installed in the country. CdTe has become the dominant source of panels in large-scale projects. The technology accounts for 55% of total solar installations in the US. First Solar has started construction of a third plant which will bring capacity to 6 GW in the country.

Toledo Solar is another US manufacturer of CdTe panels.

The law

It provides for (1) an investment of $30 billion in production tax credits to accelerate domestic manufacturing of solar panels, wind turbines, batteries and critical mineral processing.

2°) A $10 billion investment tax credit to build clean technology manufacturing facilities, including those that make electric vehicles, wind turbines and solar panels.

500 million in Defense Production Act funds for heat pumps and critical mineral processing

2 billion in grants to retool existing auto manufacturing facilities to make clean vehicles

Up to $20 billion in loans to build new clean vehicle manufacturing facilities across the US

2 billion for national laboratories to accelerate energy research.

3°) It provides a range of tax credits across the solar supply chain (see the article below for a list of tax benefits).

https://www.pv-magazine.com/2022/09/20/a-new-era-of-made-in-usa-solar/

PV Magazine of 20 September 2022

Editor's note: The magnitude of the financial support for PV manufacturers coupled with the enthusiasm of the industry heralds an American solar industrial renaissance. There are many projects for the construction or extension of factories. They will provide modern, efficient and productive equipment, at a time when the Chinese production system is based on increasing the number of jobs, and is undergoing wage increases as a result of the growing demand for employees, but without the search for productivity per employee appearing to be the dominant concern of Chinese employers.

It is very likely that the US industrial revival will only appear from 2024 onwards, when the factories start to be operational. It is also necessary to absorb the time needed to adjust equipment and to count on the increase in capacity of production lines.